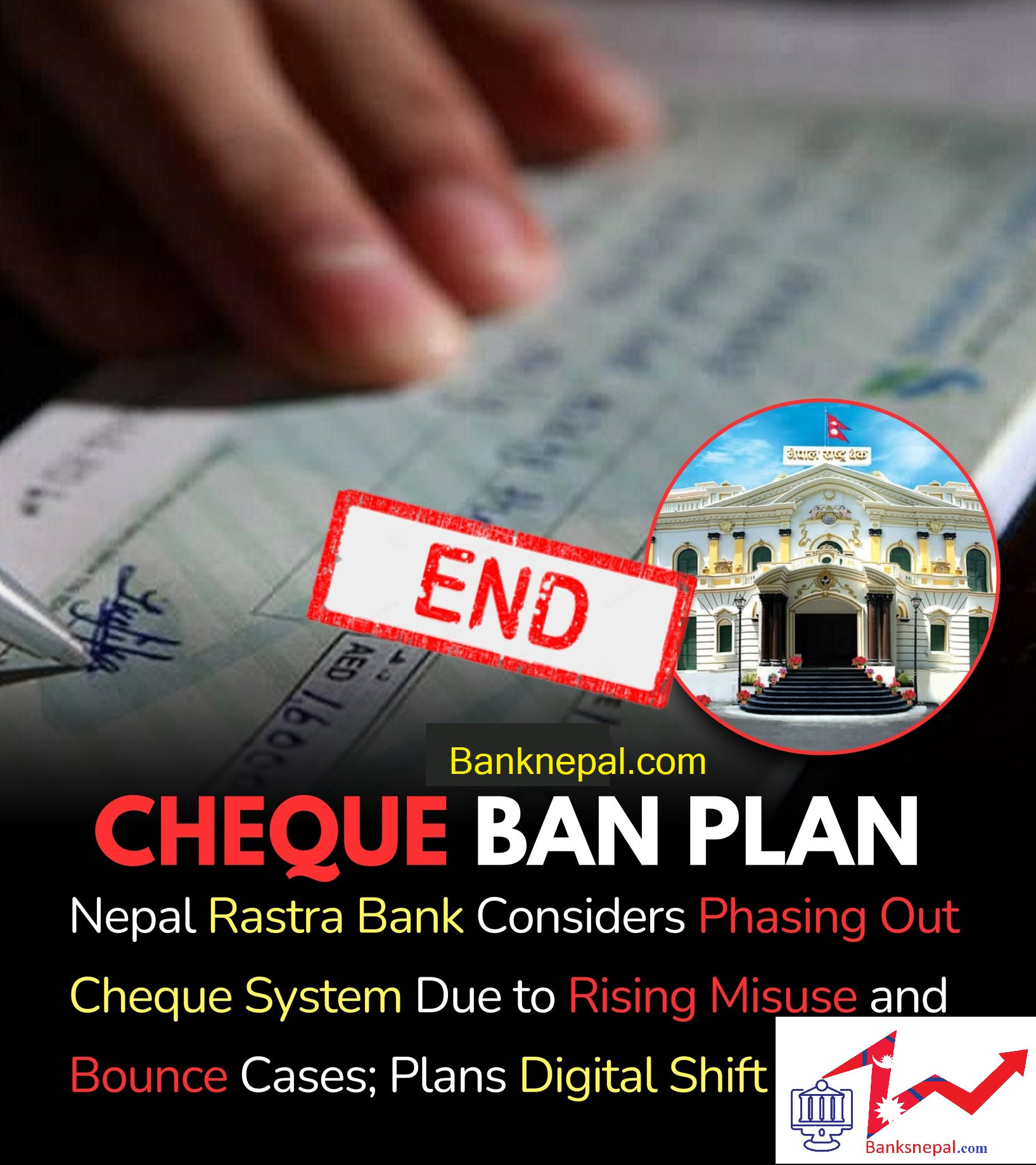

Digital Payment in Nepal : Nepal Rastra Bank is considering Banning the cheque Payment system

Kathmandu. Nepal Rastra Bank is considering gradually reducing and eventually eliminating the check system. The central bank is taking this step after the number of check bounces (dishonor) received from banks and financial institutions has increased significantly. Nepal Rastra Bank (NRB) is aggressively promoting a digital-first policy to phase out traditional paper cheques due to high misuse, rising fraud, and a shift toward electronic transactions.

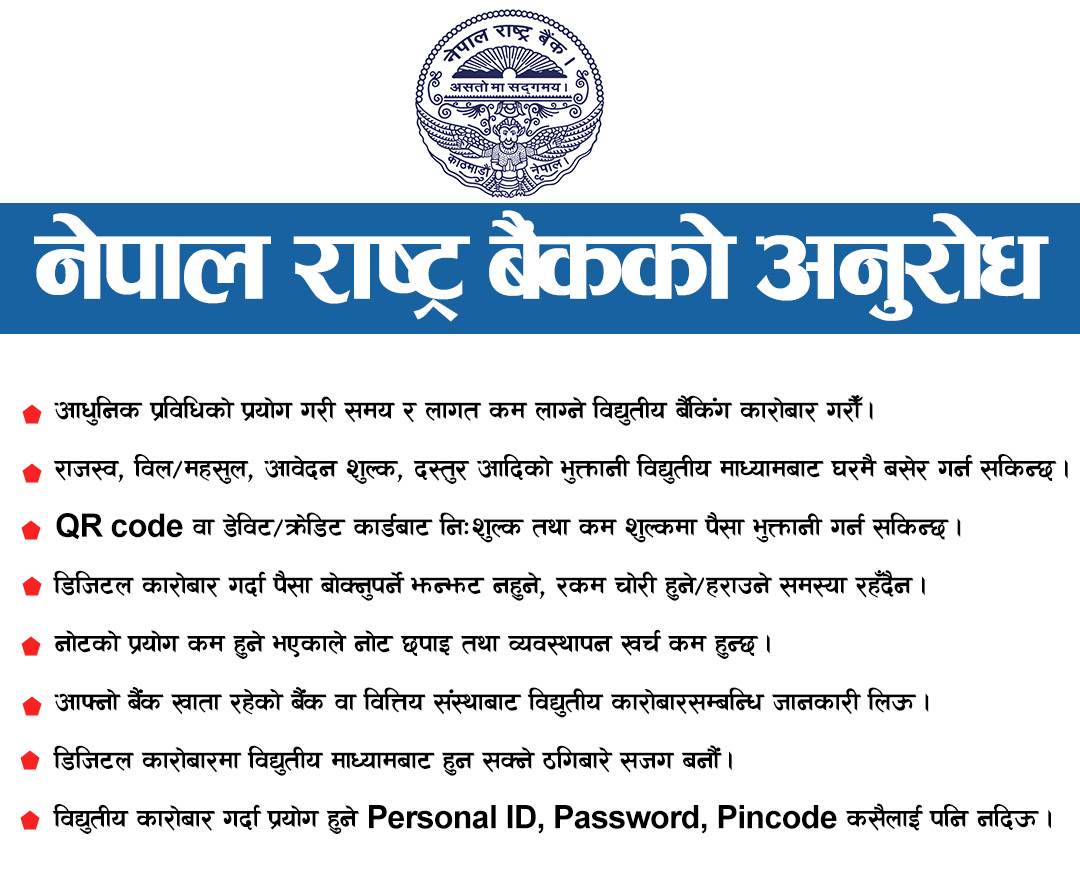

The policy focuses on strengthening digital payments (connectIPS, wallets, QR) and tightening regulations on cheque usage, including potential bans and increased oversight on post-dated cheques to curb financial crime Nepal Rastra Bank is considering scrapping the cheque system in Nepal due to increasing misuse and the rapid shift toward digital transactions. Officials say cheques are being widely used as collateral rather than for immediate payment, which goes against their intended purpose. The trend of issuing post-dated cheques without sufficient funds has also contributed to a rise in banking offenses and operational challenges.

According to recent data, a significant portion of individuals placed on the blacklist are linked to cheque dishonor cases, raising concerns about financial discipline and trust in the system. NRB is now exploring reforms, including separating blacklists for cheque bounce cases and loan defaults. Authorities are also encouraging safer alternatives like bank guarantees and formal agreements, as Nepal moves steadily toward a more secure and digital financial ecosystem.

Rastra Bank officials say — “We are thinking of eliminating the check system.” Instead, there is a plan to promote digital means such as electronic payments (e-payments), mobile wallets, and internet banking. Internet and digital literacy are still limited in Nepal, especially in rural areas and among senior citizens. If the check system is suddenly reduced, it could cause great inconvenience to small traders, farmers, and the general public.

Nepal Rastra Bank has emphasized digitalization by limiting checks, but without infrastructure (internet, power, digital devices) and public awareness campaigns, this policy may fail. Similar policy announcements have been made in the past, but implementation has been weak. Now the bank should move forward only with a phase-out plan, otherwise new problems may arise.

Related post

- डिजिटल अाईसिटि प्रा लि

- तार्केस्वर, काठमन्डौ, नेपाल

- digitalictmedia@gmail.com

© 2026 All right Reversed.Banks Nepal Pvt Ltd